Trust, transparency and retailer inertia are the key challenges to delivering a better deal for energy consumers

Every year the Australian Energy Market Commission (AEMC) shines a light on the state of retail competition in electricity and gas markets to see if small customers are having their needs met. The review looks at what’s working, what’s not, and what needs to change so customers can access deals that are best for them.

Over the past year, consumer confidence has fallen. Many factors have contributed to this – confusing bills and energy plans; and higher prices. In response consumers have taken matters into their own hands with greater uptake of new technology, and more switching between retailers and plans.

Recent retailer announcements point to flatter or falling energy prices. It is undoubtedly positive that the big retailers are passing through falling wholesale prices. It’s good news, but it’s just the beginning of what retailers need to do if they want to regain trust in the eyes of their customers.

Retailers have been slow to change with opaque and inconsistent pricing.

While some innovation is happening at the margins it is not happening fast enough for consumers wanting to take action on their energy bills.

Over the past year, hard to understand bills and offers along with the legacy effect of increases in retail electricity prices have eroded trust and weakened consumer confidence in retailers. As a result Consumers are increasingly taking matters into their own hands.

We have seen that trust has been eroded, along with weakened consumer confidence in the energy market. This has been due to hard to understand bills and higher prices which have been experienced over the past couple of years.

Over the past year:

Consumer trust in the sector fell from 50% in 2017 to 39% in 2018.

Consumer confidence that the market was working in their long-term interest fell by 10% to 25%.

Confidence in the information available to make good decisions fell by 7% to 50%.

Confidence in consumers’ own ability to make choices about the energy market fell by 11% to 58%.

Satisfaction with the level of competition fell by 6% to 43%.

Satisfaction in value for money fell by 4% to 44% for electricity.

Satisfaction in value for money fell by 4% to 60% for gas.

Consumers say they are less satisfied with the value for money in the electricity and gas sectors than they are with banking, mobile phones, internet, water and insurance services.

Annual electricity bills for the representative residential consumer increased across regions by $110 to $316 (9% to 22%), except in South East Queensland, where bills decreased by $70 (5%).

Annual gas bills for the representative residential consumer increased across regions by $14 to $192 (2% to 17%).

Small businesses faced annual electricity bill increases of between 5% and 28%.

Competition is continuing to develop

There are 16 retail gas brands and 33 retail electricity brands across jurisdictions in the national electricity market.

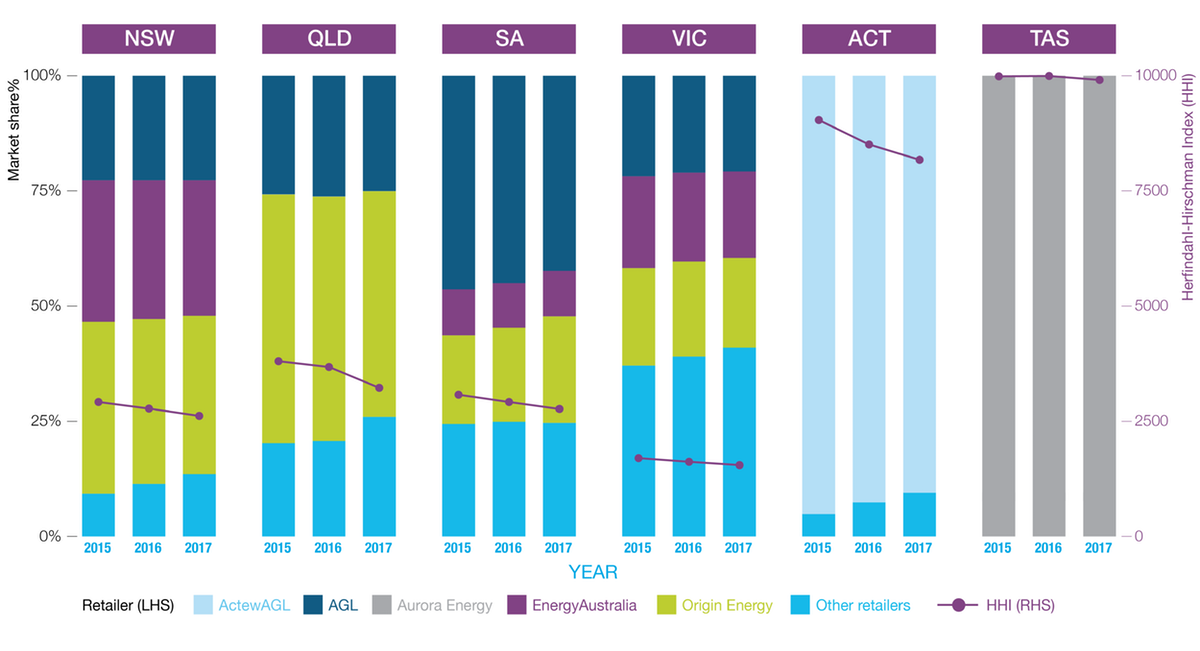

While the big 3 (Origin Energy, AGL and EnergyAustralia) maintain dominant positions in each jurisdiction, there are signs a number of electricity retailers are strengthening their competitive positions.

In jurisdictions with price deregulation the big 3’s market share continues to fall.

Second tier retailers who have generation assets underpinning their retail operations are increasing their market share, but other retailers without generation assets are finding business more difficult.

There is a structural shift underway in the market with continued growth in rooftop solar systems and the emerging growth of batteries.

Competition in action: Smaller retailers making inroads into the market share of the big 3 including Origin Energy, AGL and Energy Australia

Smaller retailers are making inroads into the market share of the big 3 in all states where there is significant competition, and the HHI index (market share) is dropping over time.

Consumers have to ask to get a better deal

It is difficult for consumers to benefit from competition in the face of complex and confusing tariff structures.

Commercial comparator sites can be helpful for customers to navigate the complex energy market. But commercial comparator sites sometimes lack transparency, and increase marketing costs for retailers.

Customers who take the initiative and threaten to change retailers are often rewarded with the best pricing. Unfortunately the opposite is also true. Loyal consumers who don’t switch are rarely offered the best energy deals.

Innovation in pricing and new products is occurring at the margins, but not fast enough.

Not enough is being done to assist vulnerable consumers in a meaningful way.

Solar is cheaper than ever and more people are installing

As the costs of solar decrease there has been a corresponding increase in installations

Australians are responding to higher energy bills and decreasing costs of solar PV systems and batteries.

The number of households with solar energy has risen again during the year under review, and more energy consumers are considering investments in batteries and other options to be more energy efficient in line with their families' needs.

There were 154,877 residential solar installations in 2017, an increase of 25% from 2016, with 1.8 million Australian households now featuring solar panels.

Consumers who installed solar have high levels of satisfaction. Between 2014 and 2016, 85% of consumers were satisfied with the installation process, and in 2016, 80% thought their system offered good value for money.

From a low base, battery installation by consumers increased by around 275% in 2017. In 2018 between 24% and 46% of customers across the national electricity market said they were considering installing batteries.

Solar PV systems are becoming more financially viable

Bloomberg New Energy Finance says 2018 is expected be the lowest cost year to install solar systems due to a combination of ongoing decreases in the cost of solar systems and government rebates. Solar PV systems now have short payback periods and a high return on investment. Modelling shows all systems have a payback period of less than nine years and a return on investment greater than 10%.

Even a 1-2 person household with low electricity usage and a small solar PV system (3kW rated output) costing $3,870 could more than halve their electricity bill in the first year. Larger solar PV systems provide even greater financial benefits for consumers.

Despite the cost of batteries falling by around 40% since 2010, battery storage systems are currently not a financially viable investment in most residential circumstances. Significant cost reductions or improvements to battery life are required to make batteries as financially attractive as solar PV.

And consumers are still seeking out a better deal

More Australians are switching their retailers and many people are using comparator websites.

Savings to be made from switching retailers increased this year in every state and territory except for electricity in NSW.

Over the past year switching rates of energy retailers increased:

over a quarter of customers in South East Queensland and Victoria changed electricity retailer

19 per cent of consumers in Victoria and 14 per cent in New South Wales changed gas retailer.

The saving from a representative residential customer switching from a median standing offer to the cheapest market offer:

on electricity, was $832 in South Australia, $574 in Victoria, $504 in South East Queensland, $365 in NSW and $273 in the ACT

on gas, was $716 in Victoria, $192 in the ACT, $185 in NSW, $161 in South Australia and $31 in South East Queensland.

Most Australians say that they would be willing to reduce their energy usage if they received an incentive to do so. Retailers are able to provide such incentives schemes, but most do not.

Retailer inaction is driving government intervention

Market reforms are supporting innovation but while some retailers have responded with new energy plans it is at the margin. Most retailers have been slow to act. In response we have seen government interventions.

Consumers find it difficult to navigate the market

Retail offers have been hard to understand, and hard to compare for some years. Despite an increase in public concern over this, coupled with an increase in focus on energy prices and bills, there has been relatively little change in the energy retail sector.

Consumers still find it difficult to navigate the market and access the best deals on offer, and retailers have done little to address this in the last 12 months.

The confusing aspects of pricing and product offering behaviour are within retailers’ control. Retailers can change their offers to make them simpler to understand. Recent interventions by governments and the increase in proposed retail rule change requests received by the AEMC are responses to retailer inaction.

There are myriad reforms in place to enable and support innovation in both technology and pricing, and to provide the necessary customer protections. Customers are starting to use them and have demonstrated a keen willingness to explore and take advantage of new opportunities in the market as they become available.

Discounts are conditional and hard to compare

Discounting remains the predominant form of competition in the retail market and remains an issue because the way discounts are offered is inconsistent across retailers, making it difficult to compare one retailer's discount with another.

Some discounts are off the whole bill, while others are off usage charges.

The conditional nature of many discounts means there can be a significant penalty if the conditions are not met. Most often, the conditions relate to on-time payments.

Of the 5,940 electricity and gas market offers that are generally available across the national electricity market-based regions, 57% of the offers have at least one conditional discount while 25% of the offers have at least one unconditional discount. Only 20% have no discounts and simply offer a price for energy usage.

Comparison websites often don’t have the best deal

Complex tariff and pricing offers from retailers have created an impetus for the growth of commercial comparator sites. These sites can assist consumers to navigate the offers in the market – helping them to understand offers and guide them through the switching process.

However, many comparator sites lack transparency about the range of offers covered, and fees and commissions paid by retailers. They may not provide the best deals to consumers. They also contribute to higher marketing costs for retailers which may be paid for by consumers.

Consumer awareness of government power bill comparison websites like Energy Made Easy remains low. Raising awareness of more trusted government sites like Energy Made Easy and Victorian Energy Compare would significantly improve consumers’ ability to access the right deal for them.

Prices are higher for consumers who don’t shop around

Retailers are increasingly focused on offering heavy discounts to consumers threatening to switch to another retailer. This, combined with confusing public offers, enables retailers to price discriminate based on how informed a customer is. This practice effectively punishes loyalty or customer disengagement.

Why smaller, innovative retailers are not doing better

Smaller retailers have driven emerging price and product innovation for consumers. Traditional retailers are slowly responding.

Over the past year smaller innovative retailers without generation assets have struggled to access affordable wholesale energy contracts and compete with larger retailers. They have questioned whether the big 3 vertically integrated retailers have faced similar high wholesale costs.

Smaller innovative retailers without generation assets see vertical integration as posing risks to wholesale contract market liquidity; their ability to access affordable wholesale contracts in the future; and minimise risk. This restricts their ability to provide value-add products and services for consumers at an affordable price.

These smaller retailers do not have generation assets, and have found it difficult to put other arrangements in place to manage higher wholesale energy costs over the past two years. As a result, over the past year these smaller, innovative retailers have struggled to compete.

Smart meters

Reforms over the past five years undertaken by energy market bodies and through stakeholders’ rule requests have improved access to smart meters, digital technologies and data, and have removed many barriers to retailers becoming more innovative and delivering better deals for consumers.

Improved access for consumers to their own data is likely to simplify the task of choosing a retailer and an energy plan in future. However retailers are responsible for the roll-out of smart meters in most places, and some customers have been experiencing delays in installations.

This review suggests some measures to increase transparency of contracts in the wholesale market with a view to improving competition at the retail level.

Rather than waiting for retailers to respond, the AEMC has made a series of reforms to help further empower consumers through its power of choice reform program. These reforms will enable consumers to demand more innovative and flexible tariffs that go beyond the current conditional discounts most favoured by retailers.

The AEMC’s new rules introducing competition in metering started on 1 December 2017. More than 500,000 smart meters have been installed since the rules were announced, and the pace of change is accelerating with 100,000 connected in the last six months.

The market operator (AEMO) and regulator (AER) are implementing the transition to smart meters. They are working closely with industry to understand why any delays are happening and how to speed up the process. The Federal Energy Minister has proposed a rule change that would require retailers to provide customers with new electricity meters within a defined timeframe. The AEMC initiated this rule change on 31 May 2018 for stakeholder consultation. A draft determination is due in September.

Different challenges are facing small and medium businesses

Small business faces unique challenges. Significant differences are emerging between small and medium businesses as they struggle with the complexity of doing business with energy retailers.

Small business trying to protect their own customers

Businesses generally consume more energy than households and pay a higher rate for their power yet there are fewer options for businesses to take control of their bills and very little access to support schemes like payment plans.

More than one-third of small businesses experienced bill shock as a result of higher energy prices over the past year.

More than half of these businesses have absorbed the price rise themselves instead of passing the burden to their own customers.

Approximately 50% have made efforts to reduce their consumption.

Only 17% looked to switch retailers.

While business customer satisfaction has been decreasing since 2016, it is now at the lowest level since the AEMC surveys began in 2014.

Retail energy price increases appear to be having a bigger impact on business bottom lines. For the first time since surveys began in 2014, businesses rated the value for money from the big 3 vertically-integrated retailers above other retailers. This suggests that retailers that are not vertically integrated have been more exposed to the increases in wholesale market costs since late 2016 and finding it harder to compete with the big 3 to make offers.

There is anecdotal evidence that the timeframe for businesses to accept bespoke electricity quotes has reduced considerably due to increased wholesale cost volatility. This makes the task of choosing the best deal harder.

Small business bills are higher than residential bills

Businesses generally consume more energy than households and pay a higher rate for their power

Bigger businesses are better equipped to deal with bill increases

There is growing diversity in how businesses are being affected by the energy market.

Businesses with more employees are better placed to deal with bill increases than smaller businesses.

Research showed:

bigger businesses are more confident in finding the right information to help choose their energy plan, and more aware of their energy consumption and management options

smaller businesses are less confident in finding the right information, have lower levels of trust in the retail energy market and are less likely to invest in new technology.

Small business owners who spoke a language other than English at home are embracing technology and renewables more than other business owners. These businesses saw greater value in renewable energy plans and access to technologies that allowed more control over their energy use, such as solar, batteries, smart meters and energy management systems.

Businesses in regional areas are taking action to reduce bills, and compared to businesses in metropolitan areas, regional businesses are more likely to:

actively investigate energy plans

have switched retailer or plan in the past five years

Higher prices and complex pricing plans are having a big impact on consumers in NSW. There are now more retailers and plans to choose from than ever before, but people are less confident they have the information they need to make decisions that are right for them.

Over the period under review, residential consumer bills increased by 9% for electricity, and 6% for gas. Small business electricity bills increased by 20%. This combined with complicated conditional offers, discounts from bases that vary by retailer, and an increasing trend towards discretionary win-back marketing created consumer confusion and dissatisfaction in NSW. The majority of consumers no longer believe that energy retailers are working in their long-term interest.

NSW customers can save between $365 to $411 off their electricity bill if they switch from the median standing offer to the cheapest market offer, which is a decrease from the previous year.

What’s happening in NSW?

The structural indicators of competition in NSW are improving. There are 28 electricity retail brands (23 retailers) and 12 gas retail brands (9 retailers). It is the second least concentrated jurisdiction. Price deregulation of the retail gas market happened during this review period on 1 July 2017.

In the past year, price rises and the complexity of retailers’ offers have seen general reductions in residential and business consumer confidence and satisfaction. Only a quarter of residential consumers believe the market is working in their long-term interests, and business satisfaction levels are at the lowest level since surveys commenced in 2014.

A number of NSW consumers have been active in taking control of their energy bills by investing in distributed energy resources. Of those customers in NSW surveyed, 26% already have a solar PV system and 24% are considering investing in a battery.

There has also been a slight increase in the past year in residential customers exploring the market in search of a better deal. Business consumers reported a significant increase in the number switching retailer or plan in the past five years, up from 52% to 76%.

Business disconnection rates in NSW were down 31 per cent in 2016-2017, prior to the recent price rises that occurred in 2017-2018, while there was a 4% increase in residential consumers on hardship programs.

Competition

Competition is increasing in NSW.

At March 2018, there were 23 electricity companies operating in NSW, up from 13 retailers since prices were deregulated in 2014. Two new retailers entered NSW in 2017; amaysim Energy and Energy Locals.

There are now nine retail gas businesses in NSW, with a number of new entrants into the gas market following price deregulation on 1 July 2017. These are Alinta Energy, Simply Energy and amaysim Energy.

NSW is the second least concentrated market in the national electricity market behind Victoria, although 86% of customers are still with the big 3.

Some retailers commented that the NSW social programs for energy code (SPC) is an additional requirement outside of the national energy customer framework (NECF) and is an example of jurisdictional divergence which may be acting as a barrier to entry.

Residential consumer bills

Residential electricity bills increased in NSW by around $111 or 9% over the past year. Depending on network region, residential consumers in NSW can save $365 to $411 off their electricity bill by moving from the median standing offer to the cheapest market offer.

While the saving from moving from a median standing offer to the cheapest market offer for electricity decreased, the maximum discount being offered for both electricity and gas in New South Wales increased over the past year. The maximum discounts off total electricity bill increased from 20% to 35%, and 27% to 32% off usage rates. The maximum discount on total gas bill increased from 18% to 20%, and off usage rates increased from 20% to 25%. Over half of big 3 electricity customers were on discounts between 11-25%, with 4% on discounts above 26%.

In 2017, switching rates for electricity increased from 17% in 2016 to 19% of all small customers.

The intention to switch energy provider or plan in the next 12 months has remained consistent at around 20% of consumers.

How residential consumers feel

Consumer sentiment is deteriorating in NSW.

Residential consumer confidence that the market is working in their long-term interests fell by 13% to 25%. The number of consumers who are not confident in the market has doubled from April 2017 to April 2018 to 40%

Consumer confidence to make good decisions about the right energy plan for them fell by 13% to 59%.

Satisfaction with both the level of competition and value for money has fallen 11% and 8% respectively to both be below 50%, consistent with the trend across all jurisdictions.

Consumer sentiment in NSW

While there has been an increase in positive sentiment in the last year, negative sentiment in NSW is significant and growing

Small business bills

Electricity bills for small businesses in NSW increased by 20% over the past year.

NSW businesses were significantly more likely to report that they have switched either their electricity/gas provider or plan in the past five years in 2018 – 76%, compared to 53% in 2017.

How small businesses feel

While the level of confidence among NSW businesses to find the right information to select a retailer or plain remained did not really change from last year, the level of satisfaction businesses have with the market fell across the board.

The level of satisfaction with current electricity provider in NSW fell 17% to 51%, the lowest level since surveys started in 2014. Average satisfaction with customer service of electricity providers fell by 8% to 58%. Satisfaction with value for money for electricity fell by 12% to 41%, and satisfaction with choice of energy companies and plans fell by 22% to 47%.

There was a 31 per cent decrease in business consumer disconnection rates in NSW in 2016-2017 from 3,107 to 2,137.

New technology

Consumers are considering other energy alternatives but are less confident that technology will be available to help them manage energy costs in the future.

The energy consumer sentiment survey from Energy Consumers Australia found that for customers in NSW, 26% surveyed already have a solar PV system, 15% are actively considering installing solar PV, and 24% are considering a battery storage system.

Electricity bills for households with solar panels are generally considerably lower than households without. The range of electricity bills for a household in New South Wales with a 3kW solar PV system, excluding the upfront cost of the system, is $446-$926 compared to $1,177-$1,982 for a household without solar.

Financial hardship

The number of customers on hardship programs (electricity and gas) as at 30 June 2017 (before the 1 July 2017 price rises), compared to 30 June 2016 increased by 4% in NSW from 31,020 to 32,231.

Electricity disconnection rates fell by nine per cent between 2015/16 and 2016/17, from 30,065 to 27,380. Gas disconnections also fell by 13% from 6,389 in 2015/16 to 5,536 in 2016/17.

NSW households have access to the means tested Family Energy Rebate, while concession card holders are also eligible for additional rebates on both electricity and reticulated natural gas. Concessions are also available for medical needs, while the Energy Accounts Payment Assistance (EAPA) Scheme provides funding to people who are in short-term financial crisis or emergency to pay their energy bills.

Government interventions

Over the past year, the NSW Government implemented three initiatives aiming to improve consumer experience in the retail energy market. This is alongside the consumer-focused interventions taken by the Commonwealth Government and market bodies.

The NSW Government’s interventions include:

proposing a rule change with the Commonwealth Government to require retailers to notify customers of price changes before they take effect (the AEMC is currently considering this proposal)

introducing its energy affordability package, which includes new rebates, the removal of retailer fees (such as late payment and exit fees), and incentives for consumers to adopt energy efficiency measures

introducing a number of new rebates as part of the NSW Social Programs for Energy Code.

Victorians continue to be the most likely to seek out a good deal and have access to the biggest discounts in any state or territory. Over the past year, consumer sentiment towards energy retailers deteriorated mainly in response to higher prices.

Complicated conditional offers, discounts from bases that vary by retailer, and an increasing trend towards discretionary win-back marketing have created consumer confusion and dissatisfaction in Victoria.

Just 26% of Victorians were confident that energy retailers are working in their long-term interest, even though more than half of all big 3 retail residential and small business customers are receiving discounts of 26% or greater on their plans.

Second tier electricity retailers have been most successful in acquiring customers in Victoria, with big 3 market share now only around 60%.

What’s happening in Victoria?

The structural indicators of competition in the Victorian energy markets are solid and show signs of improvement.

There are 21 retail businesses and 12 retail businesses. Victoria is the jurisdiction where second tier retailers have been most successful in winning market share from the big 3. It is also the only jurisdiction where most consumers have smart meters and, relatedly, it is the jurisdiction that has seen the most innovation in energy plans offered by retailers.

However, retailers claim the different regulatory arrangements that apply in Victoria compared to other jurisdictions increase their costs and in turn consumer prices.

In the past year, price rises and the complexity of retailers’ offers have seen a reduction in residential and business consumer trust, confidence and satisfaction. Some consumers have responded by investing in distributed energy resources like solar PV systems or batteries, others have explored the market in search of a better deal.

Switching rates for energy retailers have increased, with Victoria recording the highest switching rates of all jurisdictions for electricity and gas. While there are significant potential savings available between high and low offers, it’s important to consider these savings within the context of overall increased prices.

For vulnerable consumers, Victoria has the largest range of financial support programs. In 2016-2017, prior to the large increase in retail electricity prices, there was an increase in the number of consumers on hardship programs.

Competition

Competition continues to increase in Victoria - nine years after electricity and gas markets were first deregulated.

At March 2018, there were 25 retail electricity brands or 21 electricity retail companies operating in Victoria, up from 18 brands and 16 businesses in 2014.

Victoria has the highest share of second tier retailers in both the retail electricity and gas markets. In electricity only about 60% of customers are with the big 3. Victoria is the least concentrated market in the national electricity market.

Residential consumer bills

Residential electricity bills for Victorians increased by around $127 or 12% over the past year. Depending on the network area, the residential consumer can save $574 to $652 off their annual electricity bills, by switching from the median standing offer to the cheapest market offer.

Victoria recorded the highest rate of discounting for electricity across the jurisdictions, with pay on time discounts reaching 47% off usage rates and 35% off total bill for electricity. Around 50% of big 3 customers are on plans with discounts of 26% or greater, and 11% of customers receive discounts greater than 35%.

More Victorians are shopping around for the best deal than anywhere else, for both electricity and gas. In 2017, around 27% of Victorians have switched electricity retailer and 19% switched gas retailer, which are the highest rates in the country.

The number of customers indicating an intention to switch energy retailers has dropped over the last year from 24% to 22% in April 2018.

How residential consumers feel

Consumer sentiment deteriorated over the period of higher prices.

Residential consumer confidence that the energy market is working in their long-term interests fell by 11% to 26%.

Consumer confidence in their ability to make good decisions about the right energy plan for them fell by 9% to 59%.

Despite these falls, compared with other jurisdictions, Victoria continues to have one of the highest and consistent results for consumer satisfaction with the level of competition.

Consumer satisfaction with value for money of electricity has worsened over the past year by 5%, to 46%. For gas, satisfaction with value for money fell 6% to 57%.

Consumer sentiment in Victoria

While there has been an increase in positive sentiment and a decrease in negative sentiment in Victoria, the overall negative sentiment remains high

Small business bills

Electricity bills for Victorian businesses increased by around 24% over the last year.

Victorian businesses have responded by switching their retailers, reporting over the past five years an increase in switching of their:

electricity provider, up from 37% in 2017 to 60% in 2018

energy company and/or plan, up from 47% in 2017 to 74% in 2018.

How small businesses feel

Business satisfaction with their current retailer fell by 13% and satisfaction with customer service by the electricity provider decreased 10%. However, small business satisfaction with value for money of electricity increased by 10%.

New technology

The penetration of smart meters is highest in Victoria with 2.8 million meters installed across the state.

Electricity bills for households with solar panels are generally considerably lower than for households without them. The range of electricity bills for a Victorian household with a 3kW solar PV system, excluding the upfront cost of the system, is $385-$1,068 compared to $898-$1,956 for a household without solar.

Financial hardship

The number of customers on hardship programs (electricity and gas) as at June 2017 (prior to the price increases on 1 January 2018) according to the Essential Service Commission's most recent data, rose by 3% from 2016 to 32,669 in 2017.

With more households on hardship programs, electricity disconnections fell by 12% to 28,589 in 2016-2017. Gas disconnection rates also decreased by 28%, to 17,494 in 2016-2017.

Victorian households have access to the largest range of government financial assistance programs to help them manage their energy bills. The 11 programs on offer in Victoria include coverage for concession card holders, people on life support, and others with medical needs.

Government interventions

Over the past year, the Victorian Government implemented five initiatives aiming to improve consumer experience in the retail energy market. This is alongside the consumer-focused interventions taken by the Commonwealth Government and market bodies.

The Victorian Government’s interventions include:

partnering with a community organisation to design and deliver an energy brokerage service for up to 10,000 vulnerable consumers

providing a $50 bonus for each household that uses the Victorian Energy Compare website between 1 July 2018 and 21 December 2018

obtaining agreement from three large retailers to provide rebates to some customers on standing offers

commissioning the Essential Services Commission to review its regulatory codes

commissioning the Essential Services Commission to review the Victorian retail energy market and develop a methodology for a basic service offering.

The Victorian Government also awarded tenders for two large-scale batteries. These will introduce dispatchable generation into the market, with the aim of reducing wholesale costs, which in turn could have flow on benefits for retail consumers. Wholesale costs have been the main driver for the significant increases in retail prices over the past year.

Queensland has two distinct energy markets – South East Queensland where price deregulation was introduced in 2016; and regional Queensland where regulated prices are subsidised through the Uniform Tariff Policy, effectively removing competition for non-subsidised retailers.

The number of households and small businesses switching electricity plans in South East Queensland continues to rise following price deregulation in 2016 with around 25% of customers switching over the past year, up 8%.

Queenslanders are more inclined than those in other states to embrace solar PV to reduce their energy costs. Queensland has the highest rate of solar PV penetration in Australia, with a further 11% surveyed actively considering installing solar PV. Around 26% of Queenslanders are considering installing a battery storage system.

What’s happening in Queensland?

The structural indicators of competition in the retail electricity market in South East Queensland are improving, following retail price deregulation on 1 July 2016 and the market entry of Alinta in late 2017 in a 50-50 joint venture with the state-owned generator CS Energy.

Alinta has entered the market offering higher discounts than previously available. Some retailers claim this was only possible because of the joint venture with CS Energy and has created a competitive barrier to other retailers. Other retailers claim Alinta’s entry encouraged more competitive offers across the market. Regional Queensland is not an effectively competitive market and should remain regulated.

In the past year, price rises and the complexity of retailers’ offers have seen general reductions in residential and business consumer confidence and satisfaction. There has been a slight increase in satisfaction with the level of customer service in South East Queensland. These were offset by reductions in confidence that the market is working in their long term interests and their ability to make good decisions about the right energy plan. For Queensland as a whole only 21% were satisfied with the level of competition.

Queensland consumers are the most active in taking control of their energy bills by investing in distributed energy resources. It is the jurisdiction with the highest rate of solar PV system penetration, and throughout the whole of Queensland, 26% of consumers surveyed are considering investing in a battery.

There was also an increase in the switching rates of consumers, particularly in electricity in South East Queensland. There are significant potential savings available between high and low offers for electricity in South East Queensland. South East Queensland also generally experienced lower price increases than other jurisdictions in the national electricity market.

In 2016-2017, in the whole of Queensland, there were increases in the number of residential consumers on hardship programs. There was also in 2016-2017 an increase in the number of residential electricity consumers disconnected, a decrease in residential gas disconnections, and an increase in the number of small businesses disconnected for both electricity and gas.

Competition

Competition in South East Queensland is increasing with the deregulation of electricity prices on 1 July 2016.

As of March 2018, there were 18 retail companies operating in South East Queensland, up from 10 in 2014.

The whole of Queensland remains the third most concentrated market in the national electricity market, with about 86% of customers with the big 3, behind the ACT and Tasmania.

The entry of Alinta Energy in a 50/50 joint venture with the state-owned generator CS Energy in late 2017 has increased the discounts available on retail electricity plans to 28% off usage charges. Some retailers have suggested the agreement poses a barrier to retail market entry as they have been unable to access the same wholesale deal. Others have said that Alinta Energy's aggressive entry into the market is promoting competition and better price offerings to consumers.

Residential consumer bills

Residential consumer bills in South East Queensland fell by around $70 or 5% over the past year. Residential consumers in South East Queensland can save $504 or 30% off their annual electricity bill by moving from the median standing offer to the cheapest market offer.

Retailers increased the rates of discounting considerably in South East Queensland over the last year. The highest discount off electricity usage rates increased from 16% to 30%. However, 40% of big 3 customers in Queensland were on discounts between 6% to 15%.

Following market deregulation in South East Queensland on 1 July 2016, over the 2017 calendar year, switching rates for electricity increased from 17% to 25% of all small customers.

The intention to switch energy provider or plan in the next 12 months decreased by 6% over the past year to 17% in April 2018.

How residential consumers feel

Consumer confidence is deteriorating across Queensland.

Residential consumer confidence in Queensland that the energy market is working in their long-term interests fell by 10% to 21%. For South East Queensland, confidence fell 8% to 26%.

Consumer confidence to make good decisions about the right energy plan for them fell by 10% to 58% in Queensland, with South East Queensland experiencing a decrease by 3% to 65%.

However, at the same time customer satisfaction with overall service, competition and value for money improved over the year – coinciding with the fall in Queensland electricity prices for households over that period.

Overall satisfaction in customer service in Queensland is up by 5% for electricity customers and up by 5% for gas customers. In South East Queensland it is up by 6% for electricity customers and up by 2% for gas customers.

For Queensland as a whole, 25% of customers were dissatisfied with the level of competition in the market. In South East Queensland consumers satisfied with the level of competition in the market increased by 2% to 53%.

Overall satisfaction in value for money in Queensland is up by 2% to 45% for electricity customers and up by 1% to 61% for gas customers. In South East Queensland it is up by 5% to 50% for electricity customers and down by 3% to 59% for gas customers.

Consumer sentiment in Queensland

Consumer sentiment remains at low levels in Queensland despite some improvement over the last year

Small business bills

Electricity bills for small businesses in South East Queensland increased by around 5% over the past year.

Based on survey data, South East Queensland businesses who reported that they have switched either their electricity/gas provider or plan in the past five years increased to 71% in 2018 from 39% in 2017.

How small businesses feel

There was a significant decrease in confidence amongst South East Queensland businesses that they could find the right information to help them choose an energy plan. In 2018, 17% were not confident, which was an increase of 10% from the previous year. Satisfaction with current electricity retailer fell by 18% in South East Queensland, but increased by 2% in regional Queensland. Satisfaction with value for money remained around the same across both South East and regional Queensland.

There was a 17% increase in business customer disconnection rates in 2016/17 from 1,403 to 1,641. Queensland and South Australia were the only jurisdictions to see an increase in the 2017 financial year.

New technology

Consumers are considering other energy alternatives but are more reluctant than most to reduce their consumption.

Queensland and South Australia have the highest rate of solar penetration in Australia.The energy consumer sentiment survey from Energy Consumers Australia, also found that of the customers surveyed, 11% of customers in Queensland are actively considering installing solar PV and 25% are considering a battery storage system.

Electricity bills for households with solar panels are generally considerably lower than households without. The range of electricity bills for a household in South East Queensland with a 3kW solar PV system, excluding the upfront cost of the system, is $700-$1,180 compared to $1,165-$1,949 for a household without solar.

Financial hardship

The number of customers on hardship programs (electricity and gas) as at 30 June 2017 (before the 1 July 2017 price rises), compared to 30 June 2016 increased from 19,481 to 20,766. This 7% increase is the highest increase across the national electricity market, alongside Tasmania.

Electricity disconnection rates have increased in the past year by 16% (from 21,672 in 2015-16 to 25,201 in 2016-2017). However, gas disconnections fell by 30% from 1,401 in 2015-16 to 1,029 in 2016-2017.

Concession card holders are eligible for government rebates on both electricity and reticulated natural gas. Concessions are also available for medical needs, while the Home Energy Emergency Assistance Scheme provides funding to some households experiencing an emergency or short-term crisis to pay their outstanding energy bill.

Government interventions

Over the past year, the Queensland Government implemented three initiatives aiming to improve consumer experience in the retail energy market. This is alongside the consumer-focused interventions taken by the Commonwealth Government and market bodies.

The Queensland Government’s interventions include:

establishing a $21 million fund to provide households and small businesses with no-interest loans for solar or battery installations

proposing to remove its non-reversion policy in regional Queensland to allow customers who leave Ergon Energy to rejoin later

launching its affordable energy plan that includes more than $300 million in initiatives to keep electricity prices below inflation over the next two years.

In addition, in January 2017 the Queensland Government directed Stanwell Corporation to return Swanbank E gas-fired power station to service and to carry out strategies to place downward pressure on wholesale costs.

Further, in June 2017 the government directed Stanwell Corporation to change its bidding practices, to put further downward pressure on wholesale costs. Increases in wholesale costs have in been the major driver of the large increases in retail prices seen across the national electricity market over the past year

The cost of energy has led to more consumers considering different ways to save money such as more efficient appliances and battery storage. Savings available to South Australian households from switching away from the median standing offer to the cheapest market offer have almost doubled from $426 to $832 over the past year.

Residential customer bills have increased by 19% and small business bills by 24% and consumer confidence has fallen and just 24% of South Australians feel that energy retailers are working in their long-term interest.

Complicated conditional offers, discounts from bases that vary by retailer, and an increasing trend towards discretionary win-back marketing have created consumer confusion and dissatisfaction in South Australia.

The structural indicators of competition in South Australia have remained relatively stable in the past year, with the same number of electricity retailers and one new gas retailer.

Retailers continue to cite the lack of liquidity in the wholesale contracts market as a barrier to entry and expansion.

In the past year, price rises and the complexity of retailers’ offers have seen general reductions in residential and business consumer confidence and satisfaction. Less than a quarter of residential consumers consider the market is working in their long-term interests.

South Australian consumers have been active in considering distributed energy resources, with 40% surveyed already having a solar PV system and 28% considering investing in a battery. South Australia is active in harnessing distributed energy resources, with commercial and government trials of virtual power plants underway or announced.

There was a slight increase in the switching rates of residential consumers for electricity and gas, and a slight decrease for small businesses in electricity and gas. While there are significant potential savings available between high and low offers, the savings must be considered within the context of overall increased prices.

There was a slight decrease in the number of consumers on hardship programs in 2016-2017, but at that time South Australia still had the highest proportion of customers across the national electricity market on such programs. Disconnection rates increased in 2016-2017 for residential and business consumers of electricity and gas, prior to the large price increases on 1 July 2017.

Competition

The level of competition in South Australia has remained largely stable

At March 2018, there were 15 electricity companies operating, following the exit of Next Business Energy and arrival of amaysim Energy. Red Energy entered the gas market, bringing the total number of companies to six.

South Australia remains the third least concentrated market in the national electricity market (following Victoria and NSW) but has the second highest share of second tier retailers (following Victoria) with 75% of customers with the big 3.

The liquidity of the South Australian wholesale electricity market continues to be the biggest issue for retailers. Many cite the limited access to competitively priced risk management products as a significant barrier to entry or expansion in the South Australian retail electricity market. Some retailers however acknowledged that the South Australian Government’s commitment to the virtual power plant could remove some barriers to entry.

Residential consumer bills

South Australia had the largest dollar increase in residential consumer electricity bills across the national electricity market of around $316 or 19%. South Australia consumers can now though save $832 off their electricity bill by moving from the median standing offer to the cheapest market offer.

Discounts offered off total electricity bill increased in South Australia, with the maximum discount reaching 28% from 17% last year. The maximum discounts on electricity usage and gas remained around the same as last year. However, 60% of big 3 customers were on plans with discounts between 6-20%, with only 4% receiving discounts above this level.

Around the same amount of customers switched retailers between 2016 and 2017 at about 20%.

Slightly fewer consumers have indicated an intention to switch energy plan or provider in the next 12 months, 20% in 2018 compared to 23% in 2017. The main reason stated by consumers for switching was being approached by a competitor at 41%.

How residential consumers feel

Consumer sentiment is deteriorating in South Australia.

Residential consumer confidence that the market is working in their long-term interests fell by 4% to 24%.

Consumer confidence to make good decisions about the right energy plan for them fell by 7% to 62%.

Satisfaction with the level of competition remained stable, increasing slightly by 1% to 47% in 2018.

However, satisfaction with the value for money of electricity fell, by 5% in the 12 months to April 2018 to 38%, as did satisfaction with value for money of gas, falling by 7% to 53%.

Small business bills

Electricity bills for South Australian businesses increased by around 24% over the last year.

Despite this, business engagement with the electricity sector has decreased in the past year with less businesses intending to switch, or having actively investigated different energy options in the past 12 months. The number of business consumers who have switched company or plan has decreased by 3% to 19% in 2018.

Consumer sentiment in South Australia

Despite some improvement this year, consumer sentiment in South Australia is low

How small businesses feel

In 2018, 59% of South Australian businesses were confident that they could find the right information to switch, which was a drop of 11% from the previous year.

Further, South Australian businesses were considerably less satisfied with retailers across all metrics.

Satisfaction with current energy provider fell by 15% to 50%, satisfaction with customer service fell by 21% to 40%, satisfaction with value for money fell by 18% to 33% and satisfaction with choice of energy companies and plans fell by 15% to 43%.

New technology

The cost of energy is biting. Consumers are considering other energy alternatives, including more efficient appliances, solar PV and battery storage.

Alongside this, the South Australian Government has pledged to continue phase 2 of the existing virtual power plant plan, which involves the installation of 1,100 solar PV and battery systems onto housing trust properties. Phase 3 could extend this plan to 50,000 households.

Electricity bills for households with solar panels are generally considerably lower than households without. The range of electricity bills for a South Australian household with a 3kW solar PV system, excluding the upfront cost of the system, is $819-$1,363 compared to $1,467-$2,743 for a household without solar.

Financial hardship

The number of customers on hardship programs (electricity and gas) as at 30 June 2017, (before the 1 July 2017 price rises), compared to 30 June 2016 fell by 19% in South Australia from 19,274 to 15,695. While a decrease is positive, the state remains the jurisdiction with the highest proportion of electricity customers on hardship programs, with 1.51% of all electricity customers on a hardship program.

Electricity disconnection rates have remained relatively stable since 2011-12 (from 10,546 in 2015-16 to 10,902 in 2016-2017). Gas disconnections fell by almost 30% from 5,081 in 2015-16 to 3,626 in 2016-2017.

Concession card holders are eligible for government energy rebates. Concessions are also available for medical need and those living in residential parks, while the Emergency Electricity Payment Scheme provides funding to pay energy bills to householders who are in financial crisis.

Government interventions

Over the past year, the previous and current South Australian Governments implemented two initiatives aiming to improve consumer experience in the retail energy market. This was alongside the consumer-focused interventions taken by the Commonwealth Government and market bodies.

The South Australian Government’s interventions include:

committing to stage two of the previous government’s trial virtual power plant plan. Stage two involves the installation of 1,100 solar and battery systems on housing trust properties in South Australia

conducting a tender for competitive retail electricity offers for concession customers - Origin Energy was successful.

The South Australian Government also helped fund a 100MW battery, which is now operating next to the Hornsdale windfarm, and several smaller projects. These may help to place downward pressure on wholesale costs. Increases in wholesale costs have been a major driver for the large increases in retail price over the past year across the national electricity market.

Competition between energy retailers has increased and market concentration has fallen slightly, but just one in five ACT households is satisfied with the choices available when it comes to their energy provider. This is unlikely to change in the short term as a lack of effective competition in the electricity retail market means price deregulation is not an option in the short-term.

Higher prices and the complexity of retailer offers are making it hard for households and small businesses to save money. Over the past year, consumer confidence and satisfaction with the energy sector has generally fallen by more than 10% in the ACT.

What’s happening in the ACT?

The ACT is a highly concentrated market, with five electricity retailers and three gas retailers. Electricity price regulation is still in place. The retail gas market is the most concentrated amongst jurisdictions in the national electricity market.

Retailers cite electricity price regulation and the size of the market as barriers to entry.

In the past year, price rises and the complexity of retailers’ offers have seen general reductions in residential and business consumer confidence and satisfaction. Only 14% of residential consumers consider the market is working in their long term interests.

ACT consumers are the least active in seeking a better deal. In 2017, 6% of residential consumers switched electricity providers, and in April 2018, 16% of residential consumers surveyed indicated they would switch energy provider or plan over the next year. In 2018, 39% of businesses in the ACT reported they have changed energy retailer or plan in the last five years, up from 11%.

Residential energy disconnection rates in 2016-2017 increased by 10%, prior to the price rises on 1 July 2017.

Competition

The Independent Competition and Regulatory Tribunal (ICRC) regulates standing offer electricity prices for ActewAGL Retail in the ACT.

At March 2018, there were five electricity retailers operating in the ACT, consistent with previous years.

The ACT remains the second most concentrated retail electricity market, behind Tasmania, and ActewAGL has 90% of the electricity market share. The ACT has the most concentrated retail gas market amongst the jurisdictions.

Residential consumer bills

Residents in the ACT faced the largest percentage increase in electricity bills across the national electricity market of around 22% or $296 over the past year. However, households could save up to $273 off their electricity bill by moving from the median standing offer to the cheapest market offer.

The maximum discount off total electricity bills was offered for the first time at 12%, and the discount off usage rates increased from 22% to 24%. For gas, discounts off total bill were offered for the first time at 5%, and discounts off usage rates fell slightly from 17% to 16%.

Consumer engagement with the retail energy market remains low.

The ACT has the lowest level of switching in the national electricity market, but has improved steadily from 1% to 6% from 2014 to 2017.

The intention to switch electricity plan or retailer in the next 12 months was also one of the lowest in the national electricity market at 16%, although this was 4% higher than last year.

How residential consumers feel

Consumer sentiment in the ACT is deteriorating.

Consumer confidence that the retail energy market in the ACT is working in their long-term interest has halved, falling 14% in the past year to be 14% in April 2018.

Consumer confidence in their ability to make good decisions about their energy plan has also fallen by 7% in the past year to 54%.

Satisfaction with the level of competition has fallen by 17% to 20%, the lowest level of satisfaction among all jurisdictions, suggesting an appetite for more competition from ACT households.

Overall satisfaction with value for money of electricity in the ACT fell by 11% to 37%, again marking the lowest level of satisfaction in the national electricity market. Satisfaction with value for money of gas also fell 18% to 39% over the past year.

Consumer sentiment in the ACT

Despite a small increase in positive sentiment, overall consumer sentiment in the ACT is low

Small business bills

Electricity bills of small businesses in the Australian Capital Territory had the largest percentage increase across the national electricity market of 28% over the past year.

Businesses in the Australian Capital Territory were significantly more likely to report that they have switched either their electricity/gas provider or plan in the past five years in 2018 - 39 per cent, compared to 11 per cent in 2017.

How small businesses feel

Businesses in the ACT feel less confident and satisfied than last year.

Confidence businesses have in finding the right information to help them choose an energy plan decreased by 12% to 76%.

Businesses' satisfaction with their current electricity provider fell 16% to 48%, which is the lowest level since the AEMC survey started in 2014. Satisfaction with customer service of electricity providers fell by 17% to 53%. Satisfaction with value for money fell 18% to 39% and satisfaction with choice of energy companies and plans fell by 22% to 26%.

While just 23% of ACT households surveyed report having solar PV systems (the lowest surveyed figure in the national electricity market), 39% are considering purchasing them in the next 12 months (the highest level in all jurisdictions).

Similarly, the ACT has the highest number of consumers surveyed who are considering the purchase of battery storage over the next 12 months at 46%.

Electricity bills for households with solar panels are generally considerably lower than households without. The range of electricity bills for a household in the ACT with a 3kW solar PV system, excluding the upfront cost of the system, is $898-$1258 compared to $1541-$1817 for a household without solar.

Financial hardship

The number of customers on hardship programs (electricity and gas) as at 30 June 2017, compared to 30 June 2016, increased by 1% from 1,202 to 1,211.

Electricity disconnection rates have increased in the past year by 10% (from 388 in 2015-16 to 427 in 2016-2017). However, gas disconnection rates fell by 70% from 1,403 to 423.Concession card holders are eligible for payments under the Government’s Utilities Concession and Life Support Rebate.

Government interventions

Over the past year, an initiative by the ACT Government to improve consumer experience in the retail energy market was the Actsmart Solar for Low Income Households Program. With funding of $2 million over four years in the 2016-2017 budget, the program provides eligible households with a subsidy of up to 60% of the total cost of a solar system (capped at $3,000). This initiative has taken place alongside the consumer-focused actions taken by the Commonwealth Government and market bodies.

There are just two retail electricity and two retail gas businesses in Tasmania. In electricity, only Aurora Energy supplies residential customers and its retail prices are regulated.

This is unlikely to change in the short term as a lack of effective competition in the retail electricity market means electricity price deregulation is not an option.

Due to government intervention over the past year, retail electricity prices increased by only 2%. Less than 10% of Tasmanian households and small businesses are satisfied with both the level of competition and the choices available.

What’s happening in Tasmania?

Tasmania is a highly concentrated market, with two electricity retailers and two gas retailers. Electricity price regulation is still in place. Gas prices were deregulated in 2007.

Retailers cite price regulation and the size of the market as barriers to entry.

Given the government intervention over the past year capping retail price rises at 2%, Tasmanian consumers have not experienced the same large retail electricity price increases that occurred in other regions of the national electricity market.

In contrast to other jurisdictions, residential and business consumer confidence in customer service and residential value for money has increased. These increases generally bring Tasmania into line with the confidence and satisfaction results from other regions. Less than 10 per cent of residential and business consumers are satisfied with the level of competition in the energy market.

The number of residential electricity customers on hardship programs increased by seven per cent in 2016-2017, and the average debt on entry into a gas hardship program increased by around 30 per cent in the same period.

Competition

The Tasmanian Economic Regulator regulates standing offer electricity prices in Tasmania. There is no price regulation for gas.

At March 2018, there were two electricity retailers operating in Tasmania. Aurora is still the only retailer active in the jurisdiction's residential segment, while ERM Power competes with Aurora in the small business segment, though this segment represents a very small share of the total retail market. There are two gas retailers, TasGas and Aurora.

Tasmania has the most concentrated retail electricity market of the jurisdictions, and the second most concentrated gas retail market.

Retailers surveyed cited the continuation of retail electricity price regulation and the size of the market (second smallest in the national electricity market) as barriers to entry.

There is no price-based competition for residential consumers in the Tasmanian retail electricity market.

Residential consumer bills

The Tasmanian government capped the retail price increase resulting in residential customers experiencing a 2% increase in electricity bills or $37 increase over the past year.

How residential consumers feel

Consumer sentiment and engagement is very low.

Residential consumer confidence that the market is working in their long-term interests fell by 8% to 19%.

Consumer confidence to make good decisions about the right energy plan for them fell by 19% to 43%.

Confidence in the availability of information also decreased, down 10% to 42% in the past year.

Satisfaction with levels of competition in Tasmania remains low, with 9% of households in April 2018 saying they are satisfied, a decrease of 4% from the previous year.

However, satisfaction for customer service from electricity retailers was 59%, an increase of 9%, and the value for money of electricity retailers was 35%, up 1%.

Consumer sentiment in Tasmania

Despite small improvements in the last year, consumer sentiment in Tasmania remains low

Small business bills

Electricity bills of small businesses in the Tasmania had one of the smallest increases across the national electricity market of 5% over the past year.

How small businesses feel

Businesses in Tasmania are less confident, but generally more satisfied with their current electricity provider than last year.

Business confidence that they can find the right information was down by 36% to 20%.

However, business satisfaction with their current electricity provider in Tasmania increased by 14% to 82%. Further, satisfaction with customer service increased by 5% to 83%, and satisfaction with value for money increased by 7% to 87%.

Satisfaction with choice of energy company was the only metric that fell over the past year, reducing by 12% to 8%. This is not unexpected with only two retailers supplying electricity to small businesses.

New technology

The energy consumer sentiment survey from Energy Consumers Australia shows that current solar PV penetration is low. However, there is strong interest among Tasmanians for the future uptake of solar energy, with 32% of those who currently do not have solar actively considering it for the future.

While battery storage penetration is the lowest in the national electricity market at 2%, 30% of consumers surveyed stated that they are considering installing a system in the future.

Financial hardship

The number of customers on hardship programs (electricity and gas) as at 30 June 2017, compared to 30 June 2016, increased by 7% from 2,065 to 2,208. This was the largest percentage increase across the national electricity market, alongside Queensland.

Electricity disconnection rates increased by 10% in 2016-2017, from 388 to 427.

Concession card holders are eligible for payments under the government’s annual electricity concession and heating allowance, while the life support concession and medical cooling or heating concession are available to those with an approved life support system or other medical needs.

Government interventions

Over the past year, the Tasmanian Government implemented two initiatives aiming to improve consumer experience in the retail energy market. This is alongside the consumer-focused interventions taken by the Commonwealth Government and market bodies.

The Tasmanian Government’s interventions include:

introducing the energy efficiency loan scheme that provides interest free finance on a range of items including high efficiency heat pumps, solar panels, and battery storage

limiting the regulated standing offer price increase to two per cent.

Also, in November 2017, the Commonwealth and Tasmanian Governments invested $20 million in a business case study for a second Tasmanian interconnector. If progressed, it could result in additional generation in Tasmania and Victoria which would put downward pressure on wholesale costs. Increased wholesale costs have been the primary driver for increased retail prices across the national electricity market.

The right consumer protections need to be in place in the face of new technology, so that vulnerable consumers and small businesses are not left behind. This is the focus of the recommendations made by this review.

From 1 July 2018 retailers outside of Victoria will be prohibited from offering confusing retailer discounts that are higher than the retailer’s equivalent standing offer.

We are now consulting on new rules that would enable consumers to read their own meters to improve accuracy and reduce bill shock, and set minimum time frames for new smart meters to be installed. This is in addition to a detailed look into how hardship provisions can be improved to protect the community’s most vulnerable consumers.

In light of these findings, we are also recommending Victoria consider adopting the recent ‘discounting off inflated energy offers’ rule change adopted by other jurisdictions in the national electricity market to increase consumer confidence in the offers available by prohibiting energy retailers from making discounts appear bigger than they actually are.

Retailers need to increase transparency and make it easier for consumers to take action.

Reforms over the past five years improving access to smart meters, digital technologies and data have removed any barriers to retailers becoming more innovative and delivering better deals for consumers. Now the AEMC is also implementing a series of reforms to further empower consumers.

New rules around pricing network services and metering means consumers can now demand more innovative and flexible tariffs that go beyond conditional discounts.

2018 competition review recommendations

Protecting consumers

Recommendation 1: Taking into account any voluntary codes that have been developed by industry and the ECA to protect consumers receiving services from new energy service providers, the AEMC will assess whether changes to the national energy customer framework (NECF) are also required to protect these consumers. The work will commence in March 2019, unless otherwise advised by the COAG Energy Council.

Recommendation 2: The AEMC to assess how retailers support customers in financial difficulty, unless advised otherwise by the COAG Energy Council by January 2019. The review would look at the support options retailers provide commercially, and how these operate with required hardship provisions.

Enabling consumers

Recommendation 3: Retailers and comparison service providers establish an industry code of conduct for energy comparison sites and obtain ACCC authorisation for the code if necessary. The code development and any authorisation process should be funded by industry and involve representatives from consumers and other affected stakeholder groups. Failing the development of an effective code, regulatory measures may be considered.

Recommendation 4: All comparison websites should display, in a prominent location, the number of retailers and plans represented on their site as a proportion of all retailers and plans available in the consumer’s distribution area.

Improving market transparency

Recommendation 5: The AER to separately report on customer numbers, switching rates and contract type for both residential and small businesses.

Recommendation 6: The AEMC will work with industry to make data on over-the-counter electricity contracts available to the market in a form that enhances transparency of the wholesale cost of energy. This work will be done in conjunction with any proposed mechanism that would give visibility of over-the-counter contracts in the National Energy Guarantee work program.

The AEMC is very focused on least-cost solutions. We are putting structures in place that enable consumers to take control of their energy usage and bills, bearing in mind that the more costs you put into the system, the more burden there is on consumers.

Energy is one of the most important cost inputs to the Australian economy. High energy prices directly impact many parts of our economy, particularly retail and small business.

Our intention is to put the right settings in place so consumers can choose how much they want to engage with the energy market, without putting cost burdens on households and the economy that could be easily avoided with better planning and more efficient practices.

Background: This report is our fifth annual review of the state of retail competition, outcomes for small customers; and what needs to happen to enhance and improve outcomes in the future.

The review covers residential and small business consumers in retail electricity and gas markets in Queensland, New South Wales, the Australian Capital Territory, Victoria, South Australia and Tasmania.

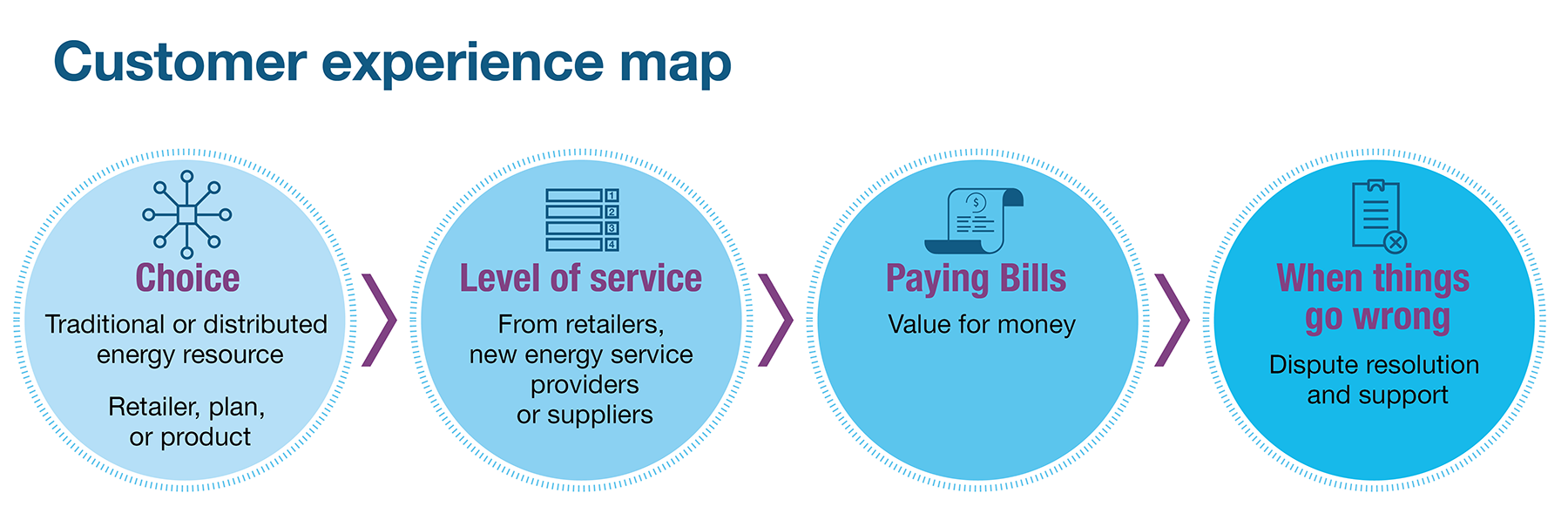

We use a number of measures to determine whether customer needs are being met, looking at the choices they have, the level of service they receive, whether they are getting value for money and what happens when things go wrong.

This year we assessed the energy consumer experience against four key dimensions - the level of choice, price, customer service and innovation. It’s a useful way to compare the experience of different consumer types, in particular customers who rely on retailer supplied electricity and consumers who invest in distributed energy resources such as solar PV and batteries.